If there is one thing those who work in mergers and acquisitions don’t like – buyers, sellers, investment bankers, and, yes, lawyers – it’s uncertainty.

However, uncertainty precisely is what has been handed to these M&A players as they start manoeuvring through a brave new world of tariffs under US President Donald Trump’s second term. It started with a bang when he signed an executive order on his first day in office decreeing a 25 percent tariff be imposed on the vast majority of Canadian (and Mexican, for that matter) goods, essentially tearing up a North American free trade agreement he had signed in his first term.

Those tariffs indeed came into effect on March 4, and there has been a rollercoaster of tariffs-on, tariffs-off since then, and much might happen by the time you read this. Still, questions remain. How long could they last? Exactly what sectors are affected? What is Canada’s response? Will both sides raise the stakes with retaliatory measures?

In this climate of uncertainty, lawyers involved in M&A and other areas are fielding questions and charged with helping their clients understand what’s going on and how it will impact their ability – and desire – to make deals.

“There’s really only one thing that is truly impacting M&A activity right now, and that is uncertainty,” says McCarthy Tétrault LLP’s Shea Small. If there was certainty about tariffs and what sectors would be affected, he says, “we could figure out how to get around it … and address it.” Small adds: “In some cases, some businesses may be drastically hurt, but others will retool and figure out a way to deal with it.” However, he says, “the fact that things keep changing” makes it hard to know how to move forward.

What makes the situation particularly frustrating for dealmakers is that 2024 turned out to be an excellent year for M&A, especially in the second half, driven by lower interest rates and lots of capital available on the balance sheet of private and strategic players. Says Small: “The thinking before all the talk of tariffs was that 2025 was going to be another good year for M&A.”

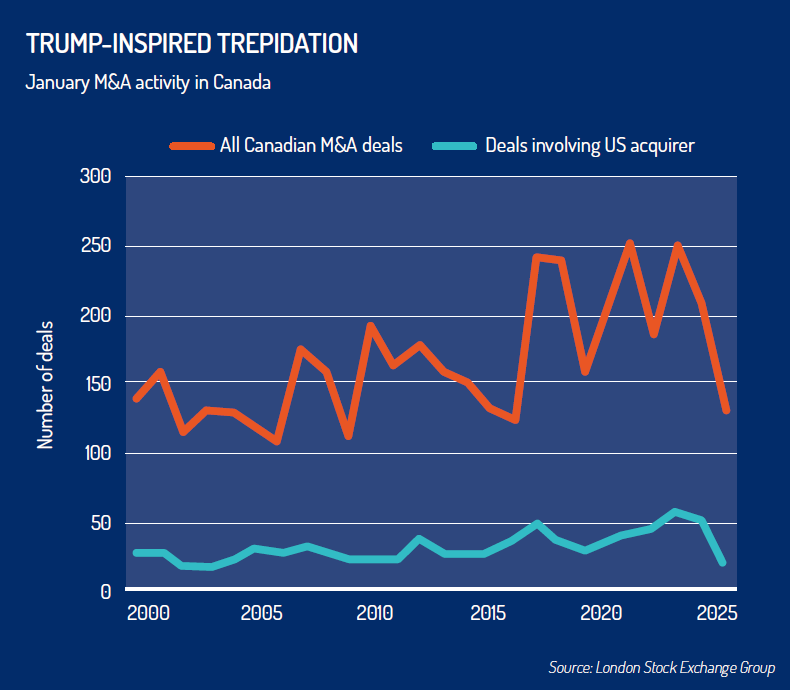

As just one insight into how the US government’s economic threats against Canada – including tariffs – have cast a pall over M&A activity, US deals for Canadian companies in January hit a 22-year low compared to the same month in previous years. According to the London Stock Exchange Group, only 19 mergers or acquisitions of Canadian companies by US acquirers occurred in January.

That compares with 50 such deals in 2024 and a 72.4 percent increase between 2020 and 2024.

Overall M&A activity in Canada also fell in January, according to LSEG, hitting a nine-year low for the month. It dropped 37 percent from January 2024, which saw 210 deals.

The overall deal value for M&A in Canada in January dropped to roughly US$6.1 billion, down from roughly US$10.1 billion in deals in January 2024. (Though that was still ahead of the US$4.6 billion and US$5 billion in January 2022 and 2023.)

Lawyers such as John Emanoilidis at Tory’s LLP say it’s “unsurprising” that dealmaking slows down during times of uncertainty.

“Generally, during periods of uncertainty, firms cut back or slow down on M&A,” he says. “It’s not all across the board, but for businesses heavily reliant on trade and exports, tariffs make it more challenging to value them. For companies with meaningful exposure to US trade, the prospect of tariffs means you’re likely looking at some discounted valuations.”

Emanoilidis points out that a seller in this situation might want to defer any transaction and is waiting for clarity on tariffs. Or if a transaction does proceed, players on both sides “will want to show greater caution as they assess the implications of tariffs.” This caution results in more due diligence, Emanoilidis says, and clients will look to lawyers to build safeguards into a deal to anticipate tariff risks.

As an example of how tariffs could impact a transaction, Marshall Eidinger, partner at Bennett Jones LLP, says: “Suppose a buyer purchases a business for $5 million, and the deal closes in six months. By then, the tariffs come in, and the margins on the product are now 40 percent less. The company is clearly not as valuable as [the buyer] thought it would be.”

Eidinger adds, “So the question becomes whether there is a mechanism in the agreement between buyer and seller to ‘true up’ the purchase price.”

It’s “not just a sell-side thing,” says Eidinger, adding that if the valuation isn’t to a seller’s liking, there’s always the option to hold off on any deal. On the buy side, “nobody wants to pay the same price for a business that isn’t as valuable as it once was.” The questions, then, turn to what safeguards are built into the contract for both sides and how to compensate if one side wants to get out of the deal.

Sarah Gingrich at Fasken Martineau DuMoulin LLP points out that while a lower Canadian dollar could spur more inbound dealmaking with Canadian assets as targets, American firms might also want to make deals here to hedge against any retaliatory tariffs that Canada might impose.

At the same time, Canadian companies could make acquisitions in the US to avoid the US tariffs on goods they manufacture. “Obviously, that may not be great for the Canadian economy,” she says. “But could it be a potential driver for dealmaking in a world with tariffs? Maybe,” says Gingrich.

However, she says, there are still far more questions than answers, and the situation seems to change daily. Gingrich notes that “the uncertainty concerns not only the impact of tariffs on a particular company or sector but also the double whammy of their effects on the markets and the dollar.”

Gingrich’s colleague at Fasken, Sean Stevens, co-leader of the firm’s corporate securities, mergers & acquisitions practice, says the uncertainty surrounding tariffs and their impact means buyers and sellers will be turning to their investment and legal advisers to find creative methods to make deals happen.

Stevens says earnouts have already been used in increasing numbers to help bridge the valuation gap between buyer and seller. However, “introducing tariffs into the equation means earnouts will likely be more complicated than what we typically see.”

He says earnouts are normally used to allow the seller to share in the business’ future value, but they will now play a more complex role in determining the risks and rewards of a deal based on the potential impact of any tariffs.

“These will be more challenging to draft, given the numerous scenarios that can play out,” he says, so lawyers will need to craft tools to balance those risks and rewards.

Like other lawyers involved in M&A, Blake, Cassels & Graydon LLP partner Cheryl Satin says the signs for 2025 point to an uptick in dealmaking over 2024, thanks to the trend toward lower interest rates and the cash that private equity and strategic players were sitting on.

But the tariff threat casts a shadow on some of that optimism, at least for the short term. “With uncertainty, it’s difficult to price a deal and determine which sectors will be most affected,” Satin says.

Still, Satin says her optimism about M&A in 2025 hasn’t taken a complete 180 turn. “We just have to have a better sense of how things will unfold so that people will be in a better position to reframe their thinking.”

She adds that while uncertainty can cause paralysis, it’s ultimately “only for a blip of time.” Whether businesses pivot their supply chains and target markets, divest non-core assets, or change geographic focus, “all these factors can breed M&A activity – businesses can’t remain stagnant.”

Blakes partner Jacob Gofman echoes Satin in saying there are still many reasons to think M&A activity will ultimately survive whatever headwinds are caused by tariffs. “There are still lots of Canadian buyers and sellers out there.

“This isn’t the first time that markets have had to deal with uncertainty and disruption,” he says. “These factors may even create new opportunities and become a catalyst for companies to reassess things and think strategically to find growth opportunities,” Gofman says. He is hopeful there will be more clarity on tariffs, but there is good reason to remain positive about mergers and acquisitions.

Another trend that Gofman expects to continue in dealmaking is “go private” transactions where publicly traded entities are taken off the market. “There’s a general perception that public companies aren’t getting the valuations they deserve in the stock market – they’re not raising equity, and they still have to incur compliance costs. This will fuel the drive to go private.”

Elliot Greenstone, a partner with Davies Ward Phillips & Vineberg LLP, says that despite the uncertainty, he remains “the eternal optimist” when it comes to dealmaking. The world has been through tough times before, the 2008 crash and, more recently, the COVID-19 pandemic, and businesses – and the economy – managed to survive.

While things might get tough, ultimately, the world goes on, he says, “and deals still need to be done.”

Greenstone also points out that the lower Canadian dollar will likely encourage foreign buyers to consider Canadian assets. The likelihood of interest rates falling to stimulate a soft economy brought on by the tariffs will also help drive M&A activity as the cost of capital becomes cheaper.

“I think you should expect to see slower deals, but not necessarily fewer deals,” he says. “People are still craving to do transactions, and there’s a good amount of dry powder there in the private equity world.”